News & Views: Open Access Charges – Continued Consolidation and Increases

Each year we survey the list Article Processing Charges (APCs) of a sample of major and significant publishers. Covering over 18,000 titles, and going back to 2016, our data set represents one of the most comprehensive reviews of open access pricing.

The latest analysis of list prices suggests prices in general are increasing, although averages for some publishers have fallen. This month, we examine the headlines and variations that lie underneath them. In the following months we will look at spreads of prices and optimization and how the competitive landscape is evolving.

Headline Changes

To compare like for like, we analyze non-discounted, CC BY charges. Overall, list prices continue to increase slowly:

- Two years ago, high-impact journals began to offer OA options, which led to above-average price increases. This year, like last year, sees overall price increases following their underlying averages.

- The highest price point for fully OA journals remains at $8,900. We now see a couple of dozen or so fully OA (“gold”) journals charging above $5,300, whereas this was the highest price for all but two last year.

- The highest price for a hybrid journal is now $11,690, up from $11,390 last year.

- Outliers aside, fully OA journal APCs are less expensive than hybrid, averaging around 59% of hybrid average APCs. Last year it was 57%; the year before 58%.

- The average hybrid APC has increased by 4.2%, compared with an average 3.5% increase last year1.

- The average fully OA APC has increased by 4.3%, compared with an average 4.1% increase last year2.

Variations by Discipline

The market-wide averages are just that: averages. They mask important variations:

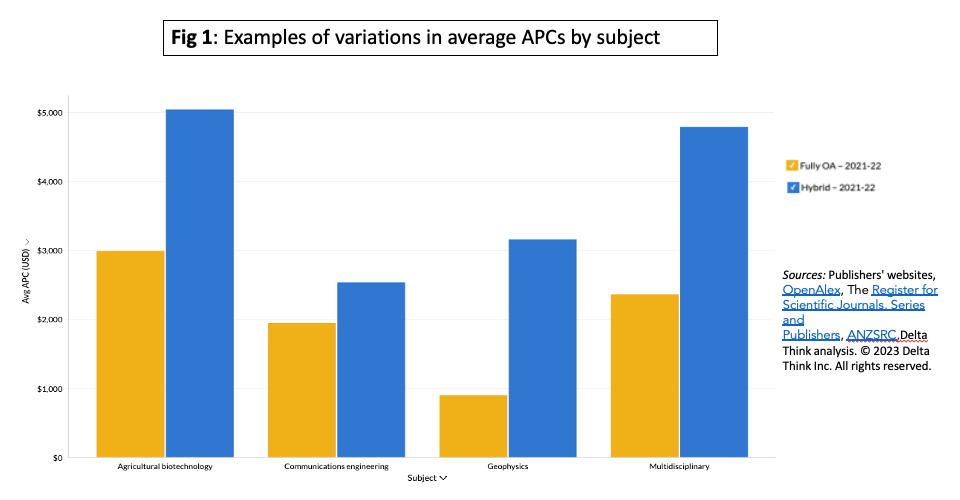

Sources: Publishers' websites, OpenAlex, The Register for Scientific Journals, Series and Publishers, ANZSRC, Delta Think analysis. © 2023 Delta Think Inc. All rights reserved.

The chart above picks out 4 of the 200 subjects we can track to illustrate the variations we see by subject. The yellow bars (left side of each pair) show average APCs of fully OA journals in the subject; the blue bars (right side of each pair) show averages for hybrid journals.

We see a big variation. For example, Geophysics averages amongst the cheapest fully OA APCs, which is less than one third of Agricultural Biotechnology, which is amongst the most expensive. For hybrids, Communications Engineering is amongst the cheapest, at under half of the average for Multidisciplinary journals, which are the most expensive.

Subject AND journal type both make a difference. For example, Geophysics may offer the cheapest fully OA prices, but it is above average for hybrid APCs.

Type of Publisher

The last few years have seen a rapid expansion in born-OA publishers, so we also examined whether their pricing is different to that of the incumbents.

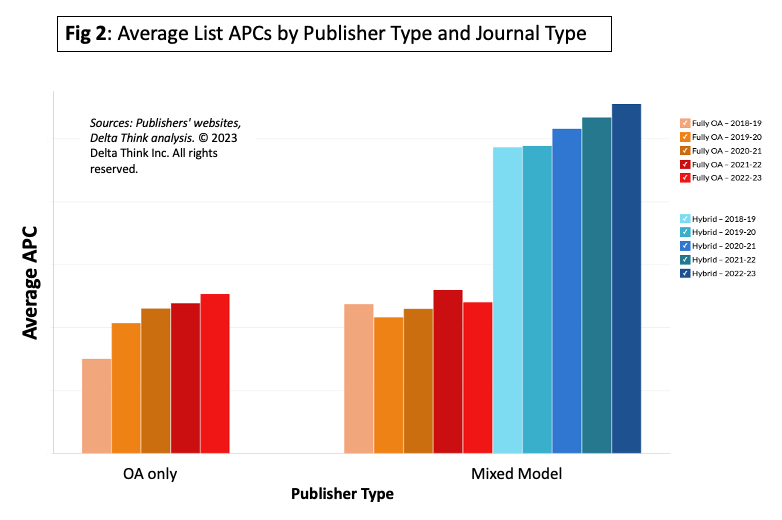

Sources: Publishers' websites, Delta Think analysis. © 2023 Delta Think Inc. All rights reserved.

Publishers that only publish fully open journals (the group of bars to the left) have historically charged lower APCs than their mixed-model siblings (shown on the right). However, the fully OA prices of the OA-only publishers have caught up over the last few years and are now slightly higher than the fully OA prices of mixed-model publishers. Although not shown here, our data allows us to separate out fully OA imprints (such as BioMed Central) from their parent publishers. These have followed similar trends to the prices of OA-only publishers but are slightly cheaper than their OA-only siblings.

We can also see the differential between higher hybrid (in blue) and fully OA prices.

Conclusion

APCs continue to rise but have settled to their long-term trends after the entrance of the expensive high-impact journals to the market a couple of years ago. Last year they rose below the average level of inflation in many countries.

Simple averages mask variations, and we see some big variations between APCs. However, the biggest predictor of price remains whether a journal is fully OA or hybrid. Additionally, while on an individual APC basis there is some overlap between the highest fully OA prices and the lowest hybrid prices, on the whole fully OA journals remain around 40% cheaper than their hybrid siblings. It also appears that born-OA prices have caught up to, and now slightly exceed, the prices of the fully OA journals in mixed model publishers’ portfolios.

A journal’s field plays a major part too, with prices showing very different averages depending on subject.

To understand the pricing of journals – whether you are setting them or paying them – it’s therefore vital to drill into the detail.

Our database tracks 18,000 prices, tracked across 200 subjects, including roll-ups into broader fields (such as Medicine or Nursing) and broad disciplines (such as Health Sciences or Life Sciences). With dozens of visualizations overlaying the data, it’s easy to put your situation in the context of the wider landscape at a glance. Please get in touch to find out more.

1In March 2022 we cited this as 3.5%. The 0.1 percentage point difference is because we have a slightly larger sample of journals this year compared with last.

2In March 2022 we cited this as 4.1%. The 0.2 percentage point difference is because we have a slightly larger sample of journals this year compared with last.

This article is © 2023 Delta Think, Inc. It is published under a Creative Commons Attribution-NonCommercial 4.0 International License. Please do get in touch if you want to use it in other contexts – we’re usually pretty accommodating.