News & Views: Open Access Charges – Consolidation, Increases, and Breaking Through the $10k Barrier

Each year we survey the list Article Processing Charges (APCs) of a sample of major and significant publishers. Covering over 18,000 titles, this represents one of the most comprehensive reviews of open access pricing.

Our market sizing has previously suggested that fully OA and hybrid prices are converging and consolidating. The latest analysis of list prices suggests that these patterns are continuing. Prices in general are increasing.

Headline Changes

To compare like for like, we analyze non-discounted, CC BY charges. Overall, list prices are increasing slowly, but with some outliers:

- The big headline is the high-impact journals now offering OA options. This has pushed maximum APCs for hybrid journals to well above their previous limits of $5,900. This year, the maximum is now $11,390 (from the Nature research journals), with the Cell titles mostly coming in at $8,900 ($9,900 for the flagship Cell).

- The highest prices for fully OA journals have risen from $5,435 to $5,560.

- Fully OA journal APCs are less expensive than hybrid, averaging around 58% of hybrid average APCs. This difference has increased a few percentage points over previous years, representing a small convergence.

- The average hybrid APC has increased by just over 5%. This is significantly larger than the 1% or so increases over the previous few years.

- The average fully OA APC has increased by 8.5% over the last year – more than twice that of previous years.

Shifts Within Portfolios

Market-wide headlines mask nuances per publisher. Most of the larger organizations have increased both fully OA and hybrid average APCs. We have discussed previously that the most important nuance lies in the spread of prices within a given publisher’s portfolio. For example, if the bulk of a publisher’s journals lie towards the lower end of its pricing, with just a few journals priced much higher, the average (mean) price will be higher than most people actually pay.

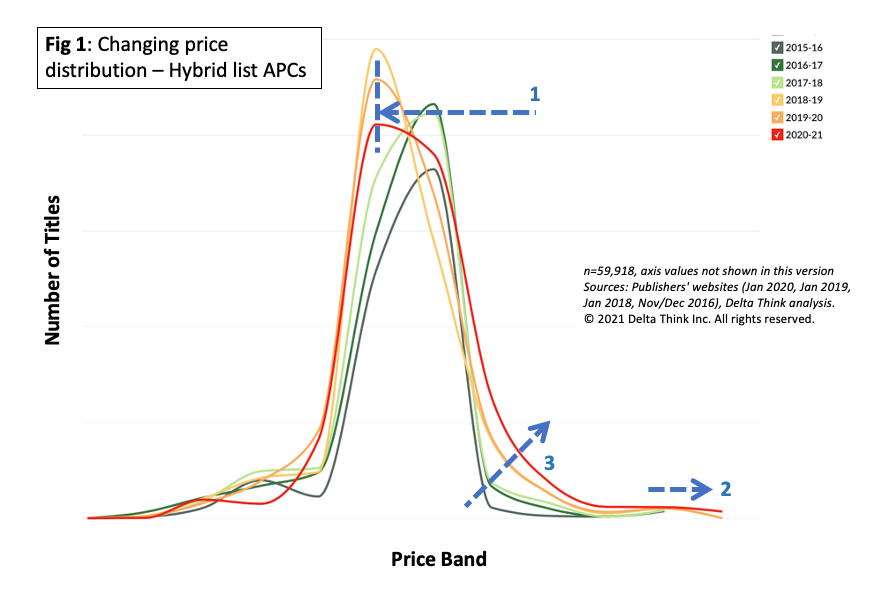

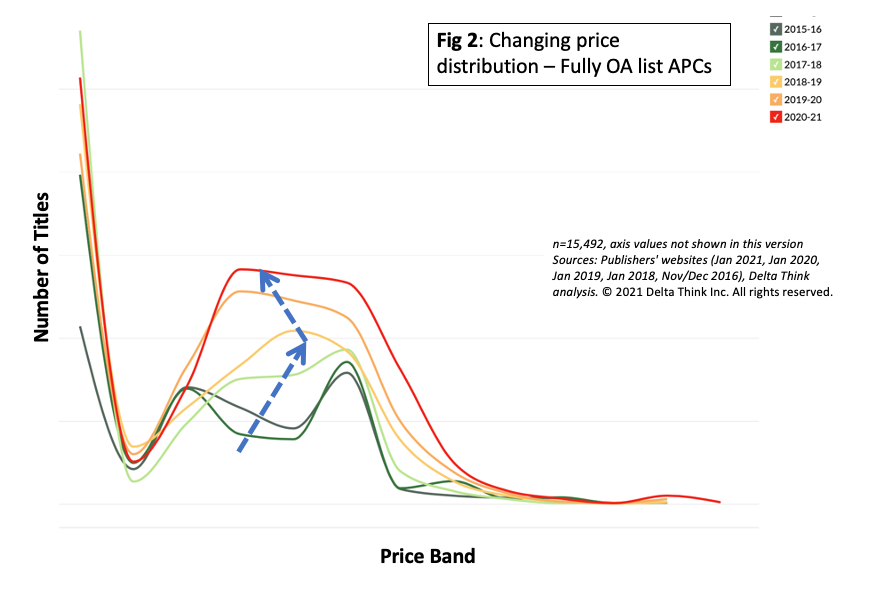

The following figures show how this plays out in the market across our sample of publishers. The figures are histograms, showing how many titles sit in various price bands over the six successive years of data that we have. For illustrative purposes, we have outlined the trends. The red line shows the most recent year’s prices. The lines become greener as they go further back in time. Subscribers to Delta Think’s Open Access Data and Analytics Tool can see full details of axes.

For hybrid journals – as shown in figure 1 below – the overall spread of prices has remained relatively constant over time. A few years ago, the most popular price band shifted slightly towards the lower end of the market (1) and has remained there since. The highest prices have increased (2 – note, for clarity, the chart combines the very highest APC bands). However, there are increasing numbers of journals at mid to high prices. Also, notice how the right-hand side of the curve is becoming shallower (3), and its tip wider. This will have the effect of increasing average prices paid, as higher APCs are becoming more prevalent.

The fully OA landscape is more complicated, as shown in Figure 2. The extreme left shows journals without APCs ($0). This significant proportion of journals are sponsored, or their APCs covered in some way that does not rely on authors arranging payments. Moving to the right, a few years ago (green lines), there was a double hump in the curve, suggesting two popular price bands. Over the last three years, the bands have merged into what amounts to a broad range of prices, with averages getting cheaper over time. As with hybrids, the popular band is widening, which will drive up the average APC paid.

Conclusion

The headline this year has been the highly selective journals offering paid OA options for the first time – and bringing with them some very high APCs. However, these outlying headlines don’t shift the market. The widening spreads of popular price bands do. As we explored at length in our analysis “APC Price Changes – When does up mean down?”, headline price rises can lead to falling overall spend or vice versa, depending on the numbers of papers published and spread of price rises across a portfolio. An important variation of this is that making a few journals slightly more expensive could drive significant extra revenues for publishers.

We should also note again that these are list prices. As mixed-model deals (RAP/PAR deals) become common, we will likely see bundled discounts emerge. In a few years, the APC market may echo the subscriptions market, where few pay the ticket price.

When we first started looking at the OA market, we noted that it was immature. The low revenues relative to subscription revenues were, we speculated, partly due to artificially low prices being deployed to promote this newer form of publishing.

The market appears to be slowly maturing and the price increases we are seeing may simply be a symptom of a market coming of age.

This article is © 2021 Delta Think, Inc. It is published under a Creative Commons Attribution-NonCommercial 4.0 International License. Please do get in touch if you want to use it in other contexts – we’re usually pretty accommodating.