News & Views: China’s New STM Policies: By the Numbers

A series of new plans and policies that could potentially impact STM publishing in China in a major way over the next few years have attracted a great deal of global attention. In this article, we take a look at the financial forces driving these policies to better understand their impact. As the vast majority of stakeholders (i.e., researchers, publishers, libraries) in the Chinese STM publishing industry are publicly funded, we treat China as one entity. The assessment looks at online publications only as the mainstream format.

Expenditure on Reading

According to the Chinese Ministry of Education, a total of 2,663 higher education institutions (HEIs) were registered in China at the end of 2018. The Steering Committee for Academic Libraries (SCAL) maintains a database and encourages members to submit data on their annual spending. According to the latest SCAL University Library Development Report, 964 libraries spent a total of $473.5m USD in 2018 to purchase electronic content, with a median spending of $155k USD. This list includes most of the top schools (66%) offering graduate programs (Tier 1) as well as some colleges (26%) without these programs (Tier 2). Assuming that all the Tier 1 schools not included in this list had spending above the median, and that all Tier 2 schools not included spent below the median, 75% of Chinese universities had less than $155k USD to spend on electronic content.

Electronic content includes everything from databases, e-journals and e-books to proceedings published both locally and by foreign organizations. For the majority of Chinese schools, the library budget is allocated first to purchase domestic Chinese language databases such as Chinese National Knowledge Interface (CNKI), which carries a price tag of 100k to several million Ren Min Bi (RMB – the official currency of China). In the case of a school with a budget below the median, once Chinese journal databases have been paid for, there is not much left to buy foreign publications. In fact, we estimate that less than 20% of Chinese university libraries buy foreign language databases.

To verify this estimate, we checked the Chinese university library consortium DRAA’s website and found that the largest consortium deal (in terms of number of members) organized for foreign language journals included 497 participants, or less than 19% of Chinese universities. This means that over 80% of Chinese universities may have access to little or no content behind a paywall, including content they themselves produced as researchers. With library budget increases at less than 3% annually (anecdotally), there is no reason to believe that this picture would change in the foreseeable future. With this in mind, it appears Open Access (OA) STM publishing would significantly benefit China.

Expenditure on Publishing

The benefit of access to research published OA is only one side of the equation. In a 2016 article, Weihong Cheng and Shengli Ren estimated that China expended a total of $72.17m USD on Article Processing Charges (APCs) in 2015. The “2020 Blue Book on China’s Scientific Journal Development” (the Blue Book1) includes an estimate of China’s APC spend in 2019 using the same methodology; it shows that China spent a total of $140m USD (average: $2,054/article) to publish OA articles in pure Gold or Hybrid journals. Although these charges may be paid by the funder, the author’s institution, or the author, this estimate assumes that the APC is paid in full at list price and that only articles with at least one Chinese funder are counted.

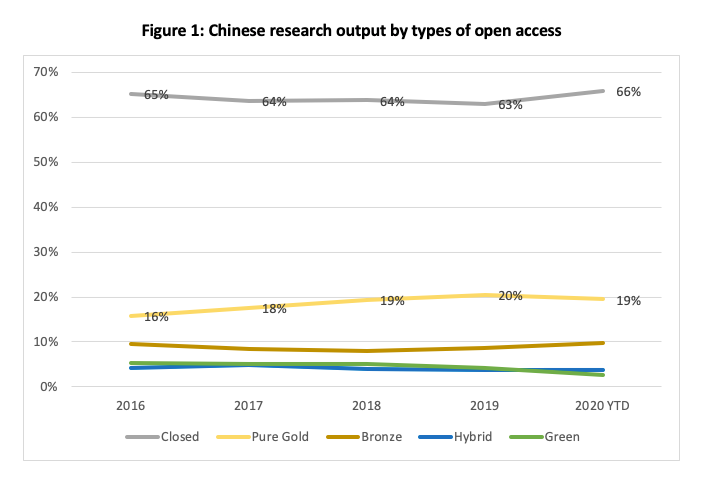

The Blue Book1 also reveals that the number of Gold OA articles produced by Chinese authors increased by 101.7% between 2016 and 2019, faster than the increase in total number of articles published by Chinese authors (65.9%). The share of Gold OA articles as components of Chinese overall research output has increased slowly but steadily over the last 5 years, as shown in the figure below.

Source: Dimensions.ai/Digital Science.

In an annualized projection (based on data from Dimensions), China is on track to publish 683k research articles (at least one of the authors’ organization is located in China) and fund more than 393k of them (at least one of the funders is a Chinese organization) in 2020. Of the 393k funded articles, fewer than 20% will likely be published in Gold and Hybrid journals.

Assuming the average cost per article remains the same as 2019, the total APC cost would be $159m USD. If all of these 393k 2020 China funded articles were published in Gold and Hybrid journals, total APC cost would surge to $808m USD. (Note: it is likely that funding information is not available for some articles and the actual number of articles funded by China is more than 393k.)

Revenue from Publishing

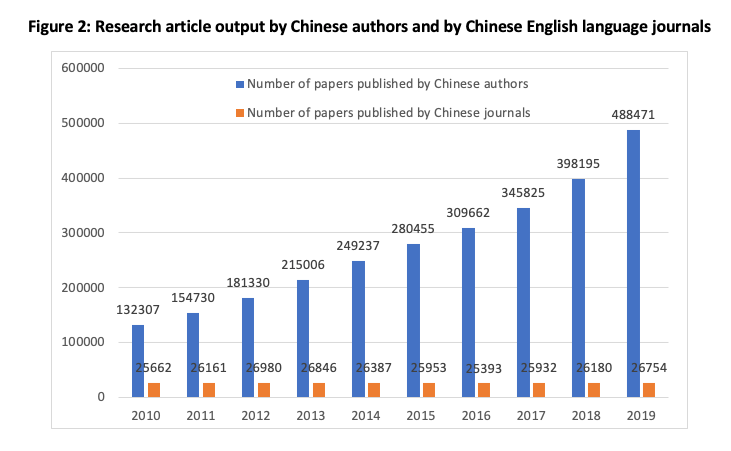

The third piece of this picture is publishers – specifically, publisher revenue. The bulk of English language STM journals published by domestic Chinese publishers are done so under a co-publishing agreement with an overseas publisher2, with revenue shared between partners. As revenue information remains unavailable, we make an educated guess on the basis of the number of published articles. A total of 359 English language titles were registered in China in 2019, of which 204 were indexed in SCI1. All the SCI indexed titles published a total of 26,754 articles1, or an average of 131 articles per title. If we do the math, the estimated total number of articles published by Chinese domestic English language titles was approximately 47k. We also know anecdotally that most of these titles are OA and, according to the Blue Book, more than 85% of the articles they published were written by Chinese authors. Again, basing our estimate on an average APC of $2,054 USD, the total revenue these titles would generate is $96.6m USD, to be shared between Chinese publishers and the international publishers they partner with.

Despite an increase in English language titles, the annual number of articles published by these titles remained nearly the same over the last decade (and decreased in some years). In contrast, articles produced by Chinese authors has been increasing rapidly, at an average annual rate of 15.7%. According to Dimensions, Chinese authors produced a total of 524k articles in 2019, resulting in a total number of articles published by domestic Chinese English language journals of less than 9% of this overall total.

The capacity of Chinese journals contrasts sharply with research output, as demonstrated by the figure below taken from the Blue Book. As the Blue Book is available in print only, the graphic above is a reproduction of the original with permission from the publisher, and with captions translated into English. Numbers shown in the graph were the numbers of articles indexed in SCI.

Source: 2020 Blue Book on China’s Scientific Journal Development (the Blue Book1).

Conclusion

Taking into account the cost of reading and publishing, compared to revenue from publishing, it is clear that while China will benefit greatly from Open Access, sufficient funding is currently not available to cover the costs of all articles when using an APC-based OA business model. Although there is great potential to increase China’s share of the global STM publishing market, it remains unclear just how to solve the inherent funding situation.

New plans and policies introduced in China recently have aimed to control and decelerate growth in article publishing cost on the one hand (setting limits on the number of qualified publications, capping publishing cost at 20k RMB per article, etc.), while growing domestic STM publishing capacity on the other (through continual financial support). The most eye-catching of these results is the mandate to publish one-third of representative articles in domestic Chinese journals, which could have the greatest impact on distribution of Chinese research by non-Chinese journals. However, China’s continued growth in R&D spending and research output could mitigate some of this reduction in distribution of research through non-Chinese publishers if overall volume continues to increase.

Dimensions shows that 2020 year-to-date article output by China is 584k and projected annual output is 683k. If Chinese 2021 output is just 600k, and one-third of these articles are published in domestic publications (assuming there is enough capacity) with a 20k RMB publishing cost cap ($3k), China could save $600m USD by publishing more of their research in domestic publications. This may be one mechanism to manage the cost of publication while also encouraging Open Access publication.

References:

1. 2020 Blue Book on China’s Scientific Journal Development, September 2020, published by Science Press on behalf of Chinese Association of Science and Technology

2. Zhang Y, Bao F, Wu J and Lin H, Reflections on the international impact of Chinese STM journals, doi: 10.1002/leap.1203, Learned Publishing 2019; 32: 126–136

This article is © 2020 Delta Think, Inc. It is published under a Creative Commons Attribution-NonCommercial 4.0 International License. Please do get in touch if you want to use it in other contexts – we’re usually pretty accommodating.